Last Month's Digest

1. The U.S. Dollar declined significantly vs. its rival currencies as a result of a global decrease in confidence in the U.S. economy.

2. Inflation took off in June, with a CPI of 2.7% compared to 2.4% in May. Potential causes include trade policies affecting expiring trade moratoriums and new tariffs being implemented.

3. Employment figures continue to impress with very positive reports in the past three months for the NonFarm jobs added figures. 150,000 on average for the April through June time period.

.

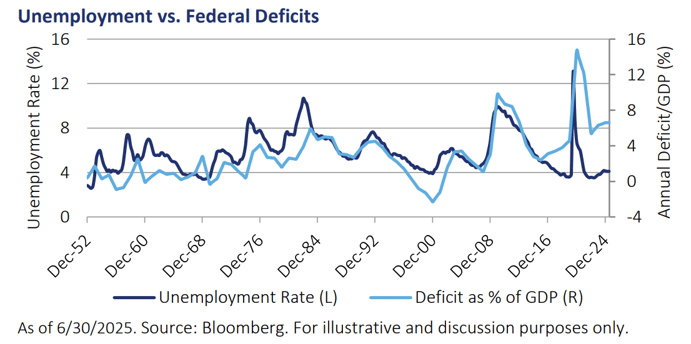

This chart visualizes how U.S. federal deficits tend to surge during economic downturns, a feature of modern fiscal policy, but also reveals a troubling pattern of deficits no longer confined to times of crisis. This could reflect deeper fiscal challenges and misalignment between spending and economic cycles.

Source: info.wilshire.com/Wilshire-Quarterly-Market-Commentary-Second-Quarter-2025

Economic Numbers

Global financial markets have been navigating a complex landscape marked by escalating geopolitical concerns in Europe and mixed economic signals from Asia. The federal reserve will meet again by the end of July and it is expected to potentially cut interest rates depending on economic indicators’ level of strength or weakness. Investors will be watching the Federal Reserve’s decision closely as well as key economic data to get a feel for future direction. Geopolitical tensions, such as the conflict between Israel and Iran, have also impacted markets, especially energy sectors.

Inflation will also be a concern as we enter the 2nd quarter of 2025. Recent figures have inflation increasing to 2.7% for the month of June. Uncertainty around this measure will play a role in the Fed’s decision to cut rates during the second half of 2025. On the other hand, a weakening U.S Dollar has presented headwinds for imports, increasing the cost of some goods as investors globally question their confidence in the U.S economy.

Despite all the uncertainty in the financial markets, the numbers have been positive for the month of June and heading into July. For example, the S&P 500, NASDAQ Composite index, and Dow Jones Industrial Average gained 5.09%, 6.64% and 4.47% respectively for the month of June, while the Bloomberg U.S. Aggregate Bond Index rose 1.54%. International markets also remained in the green for the month of June with the MSCI EAFE posting a gain of 2.2%.

Sources: Morningstar, CPI inflation report June 2025: The Dollar Has Its Worst Start to a Year Since 1973 - The New York Times, The Fed - Meeting calendars and information.

Figures to Watch

Source: Morningstar

Looking Ahead

- Tuesday, July 29, 2025. Federal Reserve meet for interest rate decision.

-

Tuesday, August 12, 2025. Consumer Price Index (inflation) report release for the month of July by the U.S. Bureau of Labor Statistics.

Login to TPFG's Advisor Resource Center

for More Indepth Coverage

Disclosures

Commentary offered in this blog is for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Any expressions or opinions reflect the views of the author and are not necessarily those of TPFG or its affiliates. TPFG does not provide tax or legal advice. Investors should consult their financial, tax or legal professionals before investing. Past performance is not a guarantee of future results. Certain information and data may be supplied by unaffiliated third parties as sourced. Although the author believes the information is reliable, we cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third party sources.

For Informational Purposes Only

PULSE 250721

CID 9639449611