Last Month’s Digest

1. Federal Reserve officials left interest rates unchanged in their March 18th meeting and continued to expect one rate cut this year as they acknowledged increased uncertainty due to conflict in the Middle East. (Source: Bloomberg)

2. The February Jobs report released by the Bureau of Labor Statistics revealed that Job openings, a measure of labor demand, decreased 358,000 to 6.882 million by the last day of February. The lowest level in nearly six years. (Source: Reuters)

3. By the end of March, the national average price for gasoline in the U.S. exceeded $4 per gallon for the first time since 2022, reflecting the pass‑through of higher crude prices from the Middle East conflict. (Source: Bloomberg)

Market Outlook

Financial markets ended March on a stronger note after a volatile month dominated by geopolitical risk and inflation concerns. Equities rebounded sharply in the final days of the period as investors responded to tentative signs of de‑escalation in the Middle East and a pullback in oil prices from recent highs. The decline in crude helped ease near‑term inflation fears, supporting a broad rally across stocks, Treasuries, and risk‑sensitive assets, even as gold prices firmed amid lingering uncertainty. On the economic front, U.S. data suggested tentative stabilization: consumer confidence improved modestly, job openings continued to cool, and hiring slowed, reinforcing the view that the labor market is losing some momentum but not collapsing. Together, these developments encouraged investors to cautiously re‑engage with risk after weeks of defensive positioning.

However, the macro backdrop remains fragile. While markets welcomed the idea that energy disruptions could eventually ease, policymakers and investors alike acknowledged that even a swift resolution to the conflict would not immediately repair damaged supply chains or restore energy flows. Gasoline prices above $4 per gallon underscore the real‑economy impact of the oil shock and present a clear headwind to consumer sentiment and spending as the second quarter begins. These pressures complicate the Federal Reserve’s task. Although officials held interest rates steady in March and continued to project one rate cut later this year, they revised inflation forecasts higher and emphasized heightened uncertainty. With goods inflation being reinforced by earlier tariffs and energy costs, policymakers signaled they need clearer evidence of inflation progress before easing policy further.

Looking ahead, markets are likely to remain highly sensitive to both geopolitical headlines and incoming economic data. A sustained rebound in risk assets will depend on tangible de‑escalation in the Middle East, relief at the gas pump, and confirmation that labor‑market cooling does not morph into broader weakness. For now, the Fed appears committed to patience, balancing downside growth risks against the danger of entrenched inflation expectations. This tension suggests continued volatility across asset classes, with equities supported by resilience in growth expectations but constrained by policy uncertainty, and bond markets oscillating between inflation scares and safe‑haven demand. As the second quarter unfolds, investors will be watching closely the energy situation, consumer spending, labor markets, and the timing of any eventual shift in monetary policy.

Sources: The Federal Reserve, Bloomberg, Morningstar, Bureau of Labor Statistics.

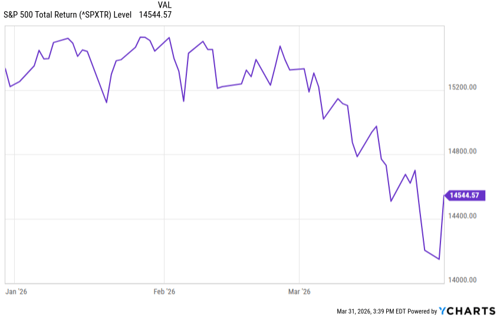

Chart of the Month

Source: YCharts

Our commentary

The S&P 500 index has reversed sharply from its mid-February 2026 highs, shedding roughly 7% YTD as geopolitical escalation in the Middle East drove oil sharply higher and triggered a classic risk-off repricing of multiples. End of March sharp vertical relief rally above the 14,500 zone signals short-covering on de-escalation headlines, but the technical picture stays cautious until energy prices stabilize and February highs are reclaimed.

Looking Ahead

- The Federal Reserve’s next FOMC policy meeting is scheduled for April 28–29, 2026.

- U.S. Q1 earnings season kicks off in mid April.

- Consumer Price Index (CPI) data for March, an important measure of inflation will be released on April 10th.

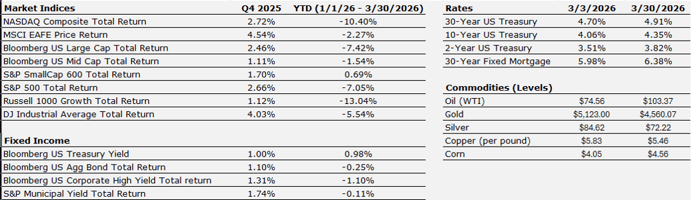

Figures to Watch

Source: Morningstar, YCharts

Disclosures

Commentary offered in this blog is for informational and educational purposes only. Opinions and forecasts regarding markets, securities, products, portfolios, or holdings are given as of the date provided and are subject to change at any time. No offer to sell, solicitation, or recommendation of any security or investment product is intended. Any expressions or opinions reflect the views of the author and are not necessarily those of TPFG or its affiliates. TPFG does not provide tax or legal advice. Investors should consult their financial, tax or legal professionals before investing. Past performance is not a guarantee of future results. Certain information and data may be supplied by unaffiliated third parties as sourced. Although the author believes the information is reliable, we cannot warrant the accuracy, timeliness or suitability of the information or materials offered by third party sources.

For Informational Purposes Only

PULSE 260331

CID 11644272911